Evaluation of Neural Network and Logit models for classification of Default in a Honduran Bank

POSTER ELECTRÓNICO

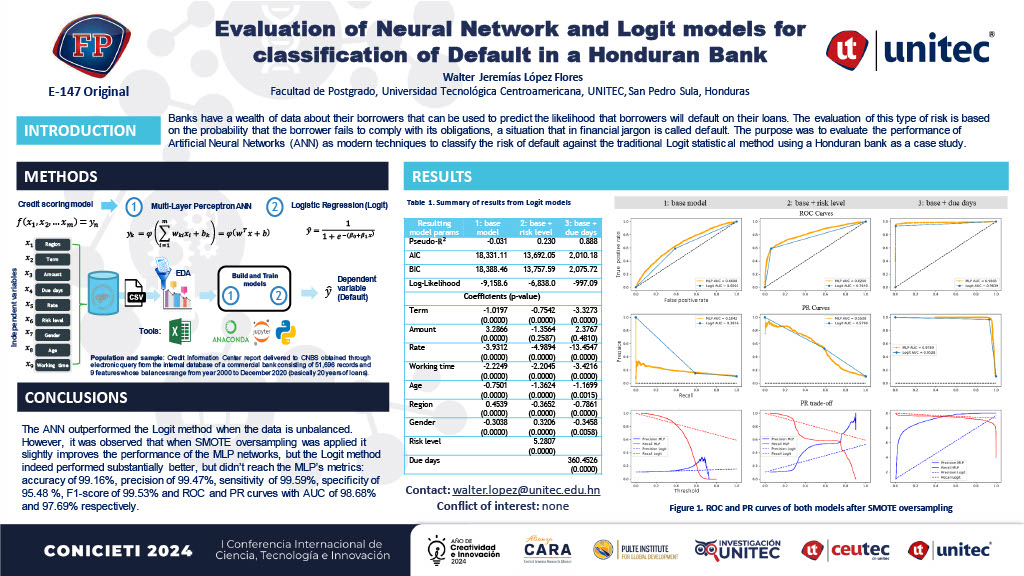

Banks have a wealth of data about their borrowers that can be used to predict the likelihood that borrowers will default on their loans. The evaluation of this type of risk is based on the probability that the borrower fails to comply with its obligations, a situation that in financial jargon is called default. The purpose was to evaluate the performance of Artificial Neural Networks (ANN) as modern techniques to classify the risk of default against the traditional Logit statistic al method using a Honduran bank as a case study.

Compartir